Summary of mandatory requirements and responsibilities

- Employers are required to make superannuation contributions in line with the Superannuation Guarantee (Administration) Act 1992 (Cth).

- Where an executive is a member of a defined benefits superannuation scheme, the employer is required to make contributions in line with the relevant legislation.

7.1 General superannuation information

Superannuation is a complex area and this Handbook does not attempt to provide advice to individuals. This Handbook outlines government policy and the choices available to employees.

A general information paper that executives may find useful is available on the VPSC website.

Which superannuation fund?

There are two types of superannuation fund: accumulation schemes and defined benefits schemes.

Accumulation schemes are lump sum funds where the investment of the individual and earnings on that investment determine the outcome for the individual on retirement. The employer contribution required under the Superannuation Guarantee (Administration) Act 1992 (Cth) is made into the accumulation fund.

The compulsory superannuation contribution is currently 10 per cent of “ordinary time earnings” (as defined for purposes of the Superannuation Guarantee legislation).

Defined benefits schemes operating in the broader Victorian public sector are closed to new membership, with the exception of the Emergency Services Superannuation Scheme which is open only to operational emergency services workers.

These schemes are established by legislation and have a prescribed level of contribution. They provide a defined benefit by way of lump sum, pension, or a combination of the two. The closed defined benefits schemes include the Revised Scheme, New Scheme, Transport Scheme and the State Employee Retirement Benefits Scheme.

Requirements for employer contributions for defined benefit schemes are available at:

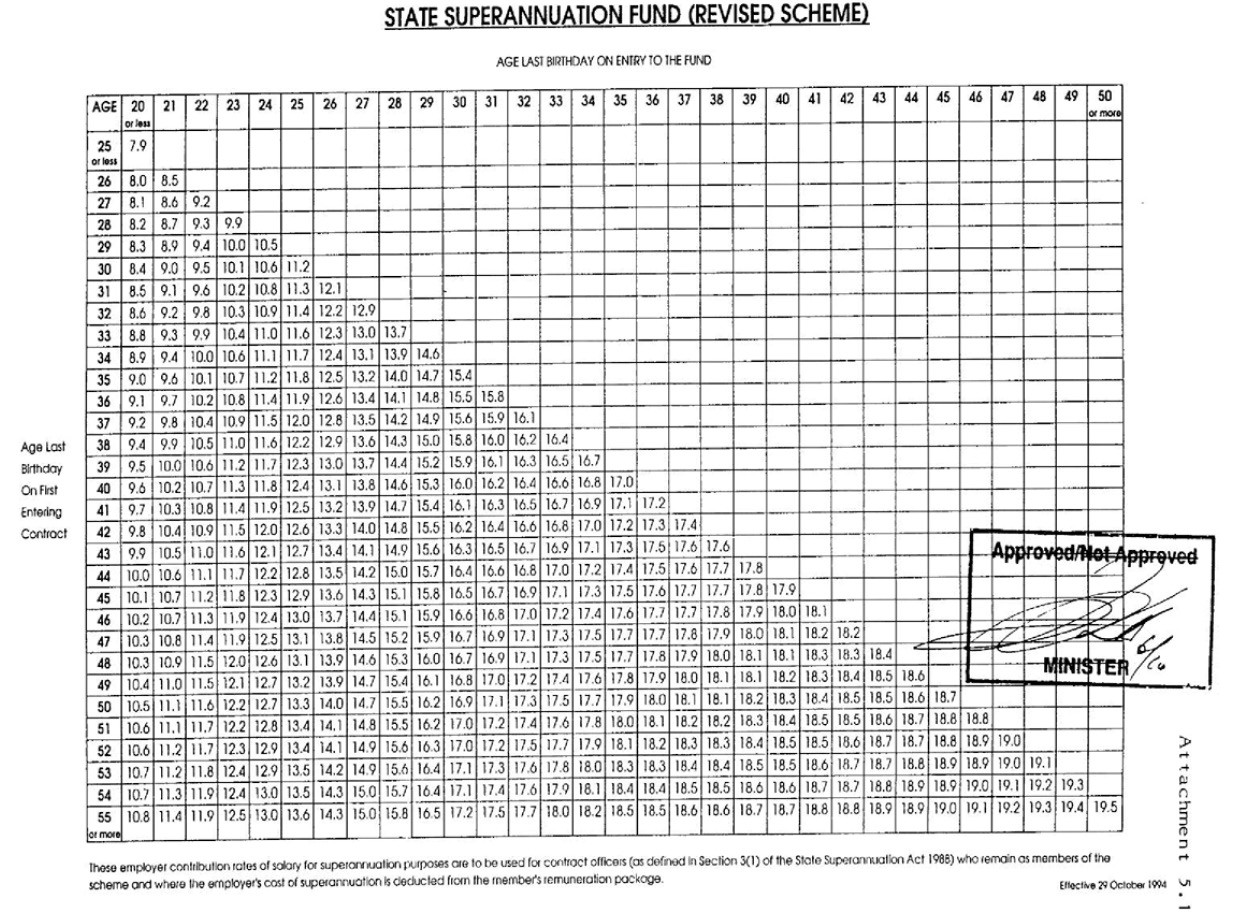

- State Superannuation Fund (Revised Scheme)

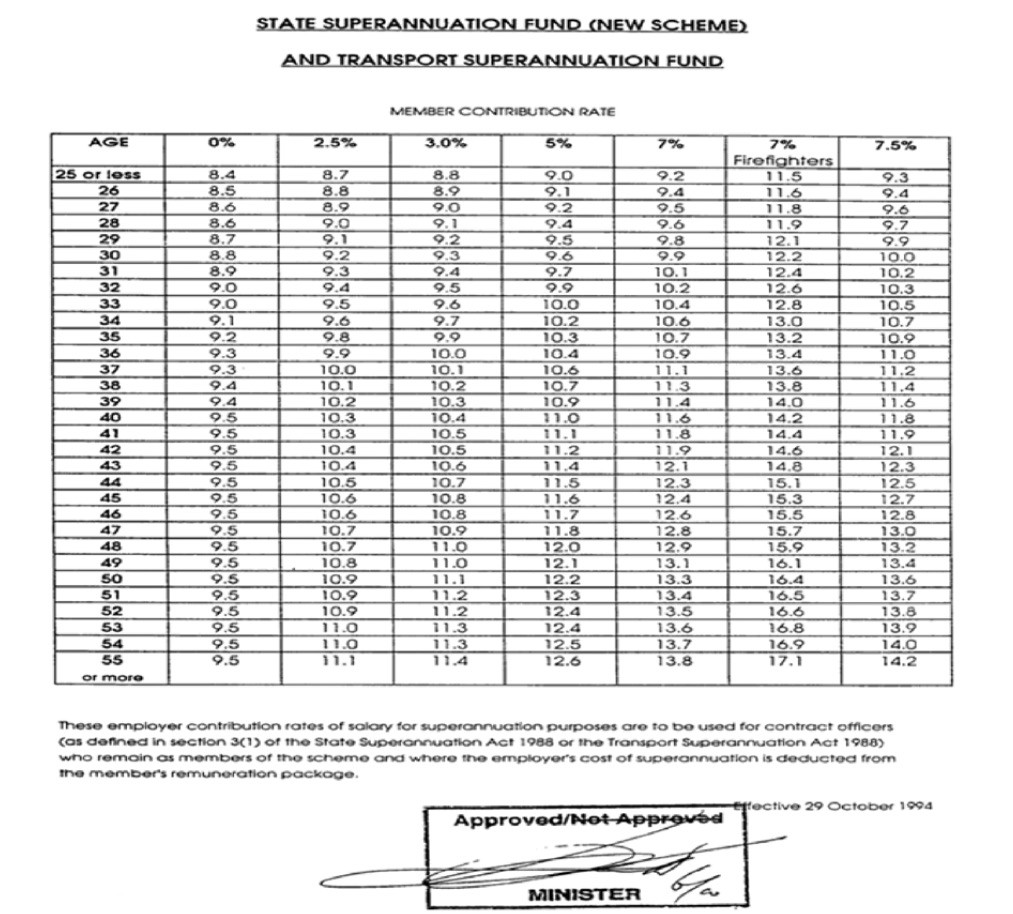

- State Superannuation Fund (New Scheme) and Transport Superannuation Fund

{kind=link}

{kind=link}

All executives are required to be members of a complying superannuation fund. However, choices are available in terms of the superannuation provider. As some executives will have been members of statutory superannuation schemes prior to entering into executive contracts the choices are complex.

Executives are required to make employer and employee superannuation contributions from their TRP if they are under a defined benefits scheme.

It is strongly recommended that executives seek financial advice before making decisions relating to superannuation.

Executives joining the public sector, or who are already a member of an accumulation scheme must ensure their scheme is a complying superannuation fund or choose a complying superannuation fund to which employer contributions can be paid. Executives are required to provide the necessary documentation to their employer to prove their fund is a complying fund if a fund other than the default fund is chosen by an individual. (Most funds provide this proof by way of a ‘complying fund status’ letter which can be easily accessed on their website.)

Emergency Services and State Superannuation can accept contributions where the executive has ceased membership of one of the defined benefit funds and still has funds with the fund.

Superable salary

Defined benefits schemes superable salary, as elected by the executive, is:

- 70 per cent of the total remuneration package

- the pre-contract superable salary, if that salary is higher.

These limits are established by State legislation in the Superannuation (Public Sector) Act 1992 (Vic) and are therefore not able to be altered in any way.

Accumulation scheme members employer contribution is calculated on the basis of a notion of salary called “ordinary time earnings” in accordance with the Superannuation Guarantee (Administration) Act 1992 (Cth).

7.2 Superannuation requirements

Employees contributing to superannuation

Employees in some public entities are able to contribute their employee contributions either after tax as a personal contribution (also called a ‘non-concessional contribution’) or before tax which can include through a salary sacrifice arrangement. Salary sacrifice contributions are considered to be employer contributions (also called ‘concessional contributions’).

The conditions for an effective salary sacrifice arrangement have been decided by ATO rulings and policy (refer to the ATO website). Executives are strongly advised to obtain independent financial advice before entering a salary sacrifice arrangement. Employers accept no liability for an executive’s decision to request a salary sacrifice arrangement.

Employee contributions to defined benefits schemes are defined in the State Superannuation Act 1988 (Vic).

Employees who are members of accumulation schemes may contribute additional voluntary contributions (whether concessional or non- concessional) subject to the rules of the relevant fund.

Limits apply with respect to concessional and non-concessional contributions. If contributions are made above these limits, additional tax may apply. Please check with the relevant superannuation scheme fund or the ATO website.

Employee responsibilities

A member of a statutory superannuation scheme, as defined in section 3 of the Superannuation (Public Sector) Act 1992 (Cth), who is about to enter an executive contract, must elect to either continue or cease to be a member of that scheme.

An executive should carefully consider their decision because once a choice has been made to cease membership of a statutory superannuation scheme that decision cannot be reversed.

The choice to remain in a statutory superannuation scheme may be changed prospectively at any time in the future.

When commencing a new contract, executives must nominate a super fund for their employer to make contributions. Executives should seek independent financial advice before making any decisions about their superannuation.

For more information about contributing towards superannuation refer to: • the VPSC website • the Emergency Services and State Super website • independent financial advice.

Lump sum payments towards superannuation

An executive may be able to make lump sum contributions directly into an accumulation superannuation fund either as a concessional contribution or a non-concessional contribution. Executives should check the rules of the relevant fund and the ATO website.

Temporary changes to remuneration (including higher duties allowance)

Where an assignment is for a period of more than 12 months, the higher level of remuneration may be included in salary for superannuation purposes in a defined benefit scheme and also will constitute “ordinary time earnings” for superannuation guarantee purposes for members of accumulation funds.

Termination benefits

Where an executive has elected to remain in a defined benefits scheme, membership of that scheme ceases on cessation of employment. The nature of any payment from the superannuation fund will be determined by the fund in accordance with the Superannuation (Public Sector) Act 1992 and will depend on the reasons for the cessation of employment.

Maximum superannuation contribution base

The amount of superannuation payable for some executives may increase each year as a result of the indexation of the maximum super contribution base (MSCB) by the Australian Taxation Office. The superannuation guarantee and MSCB apply to executives who are members of accumulation schemes. The superannuation guarantee and MSCB do not apply to executives who are members of defined benefits schemes (such as the Emergency Services and State Super Defined Benefits Scheme).

Public entity employers who use the Standard Contract must bear the cost of increases to both the superannuation guarantee and the annual ATO indexation of the MSCB. Increases to the amount of superannuation payable as a result of the MSCB indexation will be required for executives whose base salary exceeds the amount of the MSCB. Under the Standard Contract, these increases must be passed onto executives without any impact on base salary.

Public entities whose executives use another contract are required to comply with the terms of that contract. However, if there is discretion within the terms of the contract, employers are encouraged to follow the approach set out above that applies to the Standard Contract, to promote consistency across the public sector.

If an executive’s remuneration is described as: “base salary + other benefits + superannuation”, the change will be to the superannuation component only. The executive’s salary component and other benefits cannot be reduced to offset the additional superannuation payments. Employers are not to offset the cost of the changes to superannuation by passing on less of the annual adjustment to an individual executive than they otherwise would have.

Superannuation guarantee rate

The compulsory superannuation contribution is currently 10.0 per cent. There are legislated annual increases to that rate scheduled between 2021 and 2025. Those increases should be passed on to executives without any impact on base salary. More information about the dates of the increases can be viewed on the ATO website.

Mandatory superannuation contributions

Executives who are entitled to the 10.0 per cent superannuation contribution rate (accumulation fund members) are only entitled to receive contributions up to the maximum super contribution base amount which the ATO sets each year. For executives earning above the maximum superannuation contribution base, the 10.0 per cent will be capped and updated subject to indexation each year. For executives earning below the maximum superannuation contribution base, the contribution rate will be 10.0 per cent of their salary.

The monetary value of the 10.0 per cent should be updated in each executive’s contract annually where there has been any change their remuneration package to ensure they receive their mandatory superannuation contribution.